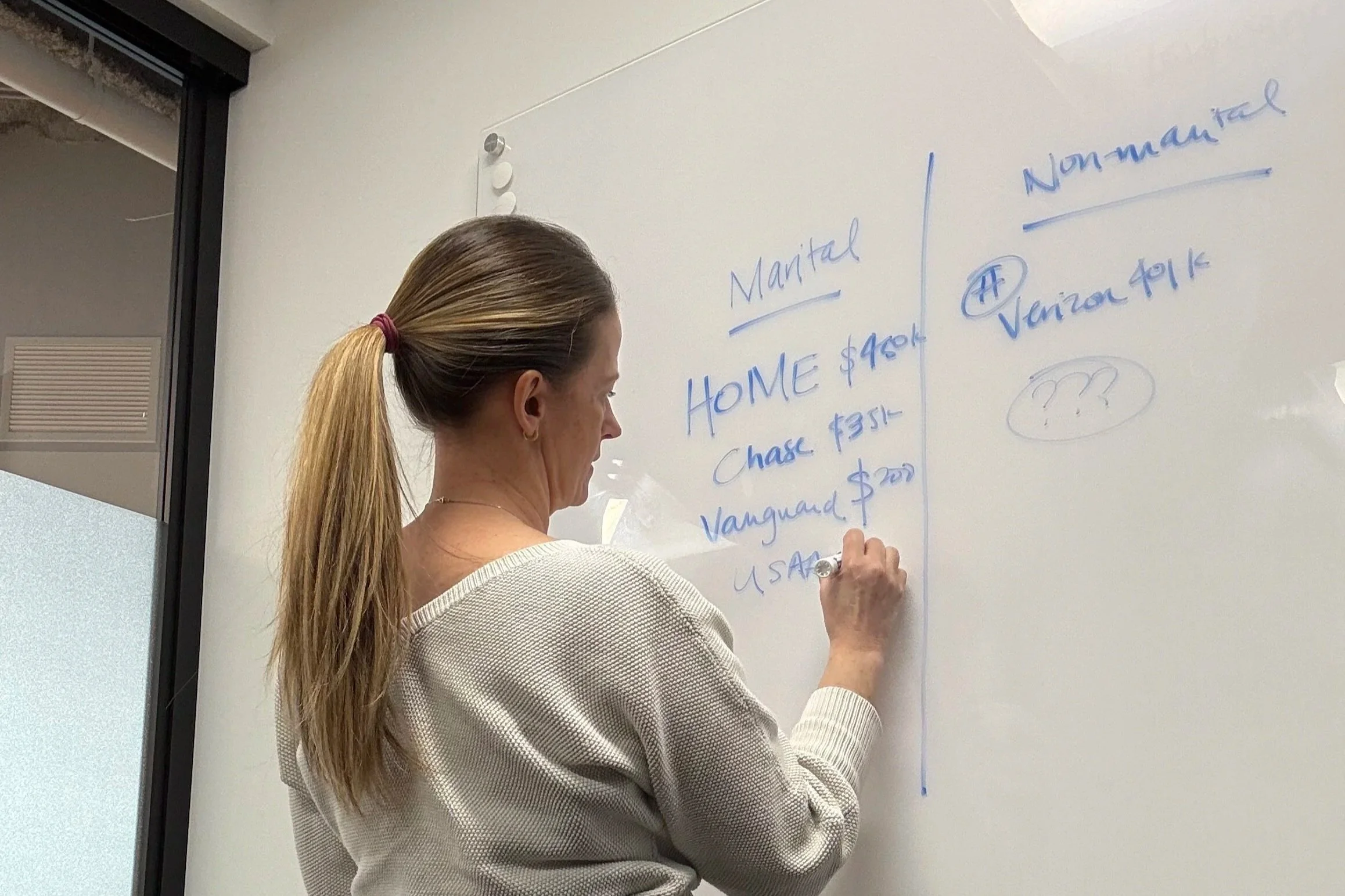

Which Assets Are Controlled by a Will and Which Are Not?

One of the most common points of confusion in estate planning is also one of the most important. Not all assets pass the same way at death, and there is no single document that controls everything. Instead, each type of asset follows its own set of rules. Retirement accounts and life insurance pass by beneficiary designation. Joint accounts and certain real estate pass by title to a surviving owner. Assets in a trust follow the terms of that trust, but only if they were properly funded into it. Everything else may pass through a will, often through probate. Most households have a mix of all of these, which is where things start to get complicated.

Each of these pathways works exactly as designed, but they do not naturally coordinate with each other. That gap is where plans can quietly drift away from what was intended. A thoughtfully drafted trust might include protections for children, but if the largest asset is a retirement account with beneficiaries listed outright, those protections never come into play. A joint account created for convenience can unintentionally override an equal distribution plan among multiple children. In both cases, nothing “went wrong” legally. The rules simply operated independently, without alignment.

These situations are more common than people expect because most planning focuses on documents in isolation. A will is drafted. A trust is created. Beneficiary forms are completed at different points in time. Accounts are retitled, sometimes partially, sometimes not at all. Over time, the plan becomes a collection of decisions made at different moments, rather than a coordinated system. The result is not necessarily failure, but it often creates confusion, imbalance, or outcomes that do not fully reflect the original intent.

This is why estate planning is not just about having the right documents in place. It is about understanding how each asset behaves and making sure those behaviors align. In my practice, this means stepping back and organizing the full picture. Each client receives a personalized roadmap that outlines what they own, how each asset transfers, which mechanism controls it, and how those pieces interact across generations. It turns something abstract into something visible and understandable, and it allows for adjustments before those rules are put into motion.

When that level of coordination is in place, the plan is more likely to function the way it was meant to. It becomes easier for the people carrying it out, and more consistent with the intentions behind it. Understanding how assets pass at death is not just a technical exercise. It is an essential part of careful legacy planning and the only way to ensure that what has been built over a lifetime moves forward with clarity and care.